At hearings before the Senate Environmental and Public Works Committee on July 18, 2013, Mr. Frank Nutter, President of the ReInsurance Association of America repeated the longstanding concerns that the Insurance industry has about climate change.

The salient point is, that Insurance companies live and die by their ability to estimate risks. To that end, they hire the world’s smartest number crunchers to figure out how much exposure they have to things like extreme weather exacerbated by climate change.

Many climate deniers claim to be “conservatives” who believe in “free market principles”. Clearly, this is not the case. If they did, they would take seriously the concerns of insurers, who actually have to respond to real world market forces. Unlike deniers, I actually believe in the power of markets, and what they tell us. If climate change does not exist, then some smart competitor will discount the “imaginary” risk of climate fueled extremes, undercut the prices of the big insurance giants, steal their business, and make them go away.

I posted some time ago on this.

Big re-insurer Munich Re (Re-insurers are companies that insurance companies go to for insurance) has been publishing their concerns about climate change hazards since 1973, and climate expert Peter Hoppe figured prominently in Welcome to the Rest of Our Lives, one of my most popular recent videos.

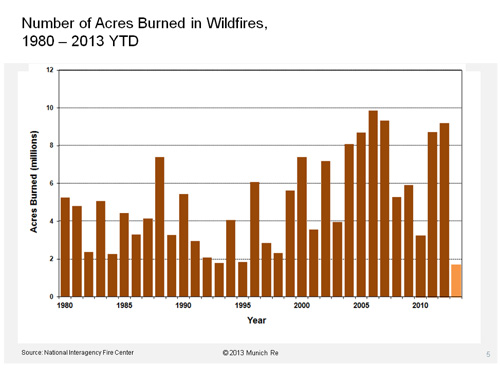

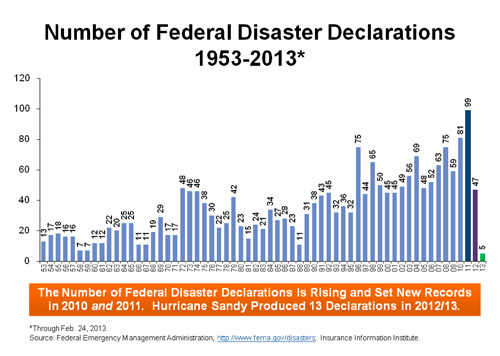

Mr. Nutter included several worthwhile warnings in his written testimony, along with revealing graphs, many from Munich Re.

Property casualty insurers are more dependent on the vagaries of climate and weather than any other financial services sector. Within the insurance sector, reinsurers have the greatest financial stake in appropriate risk assessment. The industry is at great financial peril if it does not understand global and regional climate impacts, variability and developing scientific assessment of a changing climate. Integrating this information into the insurance system is an essential function.

–Our industry is science based. Blending the actuarial sciences with the natural sciences is critical in order to provide the public with resources to recover from natural events. As the scientific community’s knowledge of changes in our climate and the resulting weather continue to develop, it is important for our communities to incorporate that information into the exposure and risk assessment process, and that it be conveyed to stakeholders, policyholders, the public and public officials that can, or should, address adaptation and mitigation alternatives. Developing an understanding about climate and its impact on droughts, heat waves, the frequency and intensity of tropical hurricanes, thunderstorms and convective events, rising sea levels and storm surge, more extreme precipitation events and flooding is critical to our role in translating the interdependencies of weather, climate risk assessment and pricing.

In the 1980’s, the average number of natural catastrophes globally was 400 events per year. In recent years, the average is 1000. Munich Re’s analysis suggests the increase is driven almost entirely by weather-related events. North America has seen a fivefold increase in the number of such events since 1980. In comparison, Europe has seen a twofold increase.

In a study on Climate Change Impacts conducted for FEMA by AECOM, the firm concluded that the typical 100 year floodplain nationally would grow by 45% and by 55% in coastal areas (with significant regional variations and assuming a fixed shoreline). Notably the report attributed 70 percent of the projected growth in 100 year floodplains to climate change and 30 percent to expected population growth (the analysis assumes 4 feet of sea level rise by the year 2100). The study recommends immediate attention to the implications for the Federal government’s National Flood Insurance Program, which is already $26 billion in debt.

Dr. David Cummins of Temple University’s School of Risk Management estimates the subsidization of disaster-prone areas embedded in Federal disaster assistance practices has encouraged development and increased Federal exposure. He estimates the expected average annual bill for Federal disaster assistance related to natural catastrophes at $20 billion. Current funding for FEMA’s Disaster Relief Fund is $1 billion. Dr. Cummins estimates this unfunded liability over the next 75 years at $1.2 to $5.7 trillion, at the high end, essentially the unfunded obligations for Social Security.

The Geneva Association (International Association for the Study of Insurance Economics) states the need for action as follows:

―The economic and social impacts of climate change could be immense; there is therefore a need for urgent and concerted mitigation action to reduce GHG emissions, supported by strong incentives from policy-makers. But regardless of the action taken to mitigate climate change, we can expect many decades of changing climate risks due to inertia within the climate system. We therefore also need concerted adaptation to avoid the predicted impacts of climate change and especially to protect the most vulnerable populations.

The massive exposure of publicly funded insurance liabilities was discussed in Jeff Goodell’s recent Rolling Stone piece, “Goodbye Miami”:

After Hurricane Andrew hit in 1992, many large insurers stopped offering property coverage in the state, citing the high risks of hurricane insurance. That left Florida in a dangerous position, with only small regional insurers to underwrite storm coverage for homeowners. But in the event of a large storm, the small insurers don’t have sufficient capital to cover the claims they would receive. To remedy the situation, the state began offering its own low-cost insurance under the name Citizens Property Insurance Corporation, which has become the largest insurer in the state. By subsidizing insurance, lawmakers hoped to keep costs down and development booming. The problem is, Florida is now on the hook for billions of dollars. “A single big storm could bankrupt the state,” says Eli Lehrer, an insurance expert and president of the R Street Institute, a conservative think tank in Washington, D.C.

Flood insurance is likely to skyrocket, too. The National Flood Insurance Program is currently more than $20 billion in debt, thanks to payouts related to Hurricane Sandy and other extreme-weather events. In 2012, Congress passed the Flood Insurance Reform Act, which jacks the price of insurance up for people living in known flood zones. More reforms of this sort are sure to come. For a place like Miami, where virtually the entire city is a flood zone, the economic costs could be in the hundreds of billions.

The financial catastrophe could play out like this: As insurance rates climb, fewer are able to afford homes. Housing prices fall, which slows development, which decreases the tax base, which makes cities and towns even less able to afford the infrastructure upgrades necessary to adapt to rising seas. The spiral continues downward. Beaches deteriorate, hotels sit empty, restaurants close. Because Miami’s largest economies are development and tourism, it’s a deadly tailspin. The threat of sea-level rise bankrupts the state even before it is wiped out by a killer storm.

And this from the Tampa Tribune:

Nationwide, the cost of homeowners insurance rose 36 percent from 2003 to 2010 — almost double the rate of inflation. Of the 15 states where rates increased the most during that time, 14 border the Gulf of Mexico or the Atlantic Ocean, according to an analysis of National Association of Insurance Commissioners figures by The Associated Press. All those states saw rates go up at least 44 percent. Rates in Florida rose 91 percent, most in the nation, while rates in Rhode Island went up 62 percent.

Industry advocates say the increases were inevitable. “Insurance rates in hurricane areas were too low for too long,” said libertarian-leaning Eli Lehrer of the Washington, D.C.-based R Street Institute.

–

Robert Hartwig, president of the industry-backed Insurance Information Institute in New York, said insurers may have sold policies cheaply to attract customers to more profitable auto and life insurance, and regulators may have been unfairly holding prices down in some states.

And, he said, claims from severe weather have gone up. The Insurance Research Council found hurricanes and other weather catastrophes caused 39 percent of nationwide homeowners insurance claims payments from 2004 to 2011, compared with 25 percent from 1997 to 2003.

Below, Peter Hoeppe of Munich Re discusses Climate risk management.

asking insurers if risks should be considered higher is like asking scientists if more money should be allocated to research -the answer is often very obvious

in the reinsurance business furthermore there are three giants. One is totally committed to the cause (Munich Re), one is lukewarm (Swiss! Re) and the other doesn’t care a jot about climate change. So far.

the market will shake them out.

Flood is a type of natural disasters which comes uncertain and can wipe out even the whole village, the slaughter which is cause by the flood is counted in insurance and one can get claim from there to start a new live. If the claim and still you are genuine and wanted your own money from insurance company then some loss assessors help to get that.

Reference:-

http://www.balcombes.ie/services/flood-water-damage/

Climate change stands to increase insured losses. With high risk of hurricanes, tornadoes, floods and wildfires on particular areas, large insurance companies stopped offering property coverage. But it is actually the lack of action to combat climate change that is the true threat to the insurance industry.

If you are looking for an insurance company who offers different personal and business insurance policies, I recommend Marchionne Insurance. I was able to get a car insurance in Wilmington MA with the best coverage at a reasonable price.